Väljalogimine

Logi sisse

Q1 2026 was, by almost any measure, one of the most challenging quarters the cryptocurrency market has endured since the bear market of 2022. Bitcoin — the market's most visible benchmark and the world's largest digital asset by market capitalisation — fell approximately 47% from its October 2025 all-time high of $126,000. Within Q1 itself, BTC shed roughly 25% of its value, from approximately $88,500 at the start of January to around $65,000–$70,000 by late March, with an intra-quarter trough near $60,000 reached in early February. Altcoins broadly amplified these losses. The total crypto market capitalisation contracted sharply. Fear & Greed Index readings remained locked in Extreme Fear territory for 46 consecutive days. By any conventional measure, the digital asset space was in deep distress.

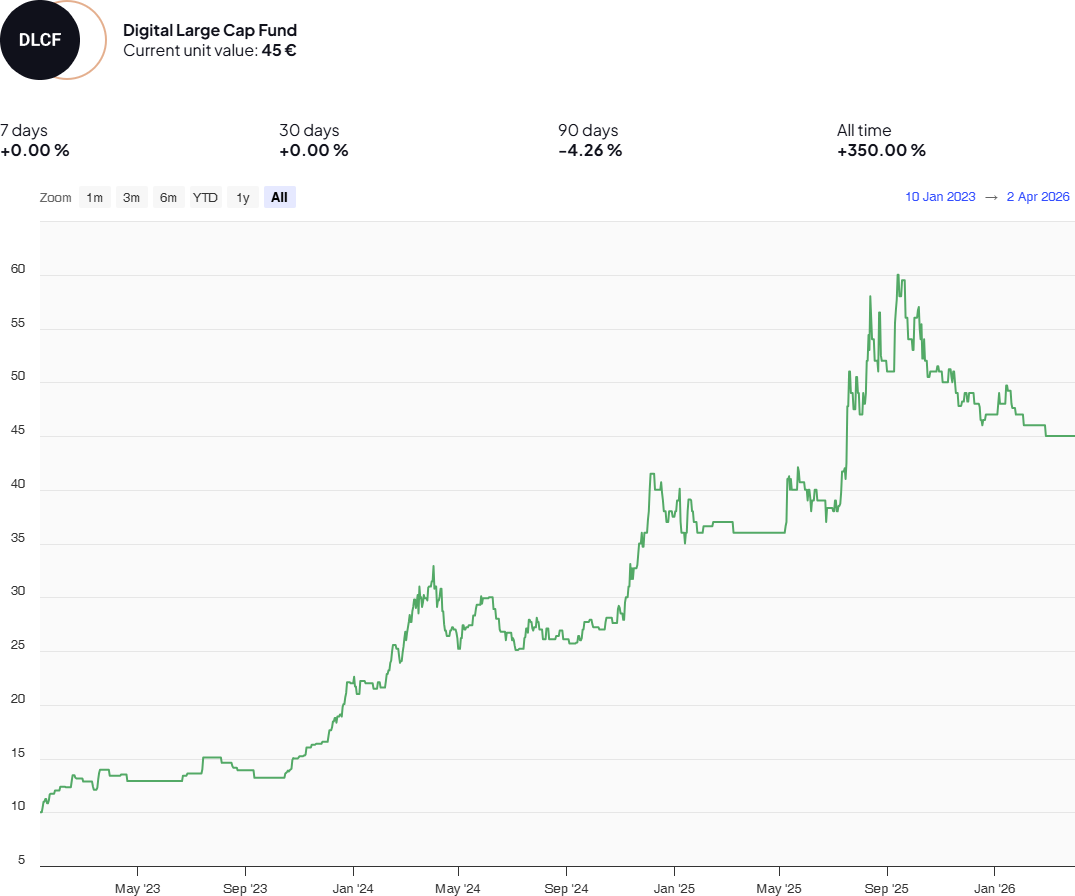

Against this backdrop, the Geco Capital Digital Large Cap Fund (DLCF) delivered a performance that stands in sharp and striking contrast to the broader market. The fund's unit value declined from €47.00 at the start of Q1 2026 to €45.00 by quarter-end — a drawdown of just 4.26%. While a decline of any magnitude is never a cause for celebration in isolation, the critical context is the magnitude of the loss relative to the storm through which the fund navigated. Where Bitcoin lost approximately a quarter of its value in the same quarter, DLCF preserved 95.74% of investor capital. That differential is not a matter of luck. It is the product of deliberate strategy, experienced active management, intelligent portfolio construction, and disciplined risk management.

DLCF -4.26% vs Bitcoin -25%+ in Q1 2026. A capital preservation ratio of 5:1 in one of the worst crypto quarters in recent history.

This report examines that performance in detail. It traces the anatomy of the Q1 2026 crypto market crisis month by month, analyses the specific macro forces and on-chain dynamics that drove the downturn, and then dissects how DLCF's portfolio design and active management approach translated into the fund's resilience. It closes with a forward-looking perspective on what the Q1 experience reveals about the DLCF investment philosophy and its positioning for the recovery phase ahead.

Bitcoin entered 2026 at approximately $88,500, carrying the residual momentum of the October 2025 all-time high alongside the cautious optimism of institutional investors still committed to the asset class. Prominent voices in the industry were bullish. Analyst Tom Lee of Fundstrat publicly called for a new all-time high before the end of January. James Butterfill of CoinShares projected a 2026 range of $120,000–$170,000. Bitcoin spot ETFs attracted an estimated $760 million in net inflows in a single day in mid-January, with Fidelity's FBTC product alone accounting for over $350 million.

On January 14th, Bitcoin hit its Q1 peak of $97,838 — just shy of the psychologically significant $100,000 level, and a level that marked a structural higher-high on the medium-term chart. The recovery narrative appeared intact. Then, without warning, the second act began.

A meltdown in Japan's government bond market on January 20th triggered a sudden, global risk-off sentiment event. The Trump administration's escalating tariff threats against the European Union added policy uncertainty. The Senate Banking Committee's long-anticipated markup of the CLARITY Act — legislation the crypto industry had been lobbying for to establish a clear regulatory framework — was abruptly postponed after Coinbase withdrew support over a dispute about stablecoin yield restrictions. Institutional confidence cracked. By January 31st, Bitcoin had fallen to $75,993. The peak-to-trough drawdown within January alone was 22.3%. Estimated 24-hour liquidations on January 31st alone exceeded $2.56 billion, almost entirely concentrated in leveraged long positions.

Bitcoin spot ETFs — which had attracted $1.9 billion in net inflows during the first week of January — swung to net outflows of $1.61 billion for the month in total. Whale-tier on-chain wallets, holders of large Bitcoin positions, were found to be selling into January's rally while retail investors were buying. This divergence between smart money and retail behaviour was one of the clearest warning signals that the recovery lacked conviction at the institutional level.

If January felt like a warning, February delivered the reckoning. On February 5th, Bitcoin registered one of the most statistically extreme single-day price moves in the asset's history: a -6.05 standard deviation event on the rate-of-change Z-score, as documented by VanEck's digital assets research team. In plain terms, this was a crash that dwarfed normal market volatility by an extraordinary magnitude. In the span of approximately ten trading days, Bitcoin plunged 32% from its January closing levels, retesting and briefly touching the $60,000 psychological support zone on February 6th.

From there, BTC entered a prolonged, grinding consolidation range: support between $63,000 and $65,000, resistance capping recovery attempts at $69,000 to $70,000. Every time buyers attempted to push prices higher, sellers reasserted. Ethereum mirrored this pattern, falling to a local low of $1,750 before consolidating between $1,800 and $2,000. The broader market cap shrank sharply.

The causes of February's collapse were systemic. The U.S. Federal Reserve, confronted with sticky inflation refusing to return cleanly to its 2% target, maintained elevated interest rates and pushed back market expectations for rate cuts well into the second half of 2026, if not 2027. The higher-for-longer rate environment raised the cost of carry for speculative assets and encouraged capital rotation into yield-bearing fixed income instruments. Geopolitical tensions in the Middle East escalated meaningfully, generating energy supply uncertainty and global risk-off flows. AI sector anxiety — the fear that artificial intelligence could compress margins across the technology sector — caused aggressive selling in U.S. tech stocks, which dragged Bitcoin lower with it, as many post-ETF institutional portfolios now treat Bitcoin and software equities as correlated components of the same risk factor.

Bitcoin miners added incremental selling pressure as falling prices compressed profitability, forcing some operations to liquidate holdings to meet operational expenses. The Bitcoin network hash rate declined as a result. ETF flows for February showed net outflows of $206.52 million — a significant reduction from November's $3.48 billion peak outflow, suggesting institutional deleveraging was nearing exhaustion. But the damage to sentiment was profound: the Fear & Greed Index entered Extreme Fear territory and would remain there for 46 consecutive days across February and into March.

March arrived with crypto markets bruised and investor sentiment at historically bearish levels. Polymarket prediction market data showed approximately 62% of participants pricing in Bitcoin falling below $50,000 at some point in 2026 — a remarkable bearish consensus for an asset that had been trading above $100,000 just months earlier. The Fear & Greed Index, while no longer at its absolute lows, remained far below levels historically associated with sustainable recoveries.

Price action told a story of halting, contested stabilisation. Bitcoin gradually reclaimed ground from the February lows, trading near $70,416 on March 20th — a meaningful bounce, but one met at every step by resistance. The Federal Reserve's FOMC meeting on March 17th produced a textbook sell-the-news outcome: Bitcoin rallied to a pre-announcement high of approximately $74,000, then fell back to $70,500 after the Fed's dot plot reaffirmed a restrictive stance. The 10-year U.S. Treasury yield held near 4.42%. President Trump publicly pressured the Fed for lower rates and zero inflation, but the central bank's operational independence meant these calls had no immediate market impact.

In the final week of March, fresh 15% global tariffs announced by the Trump administration triggered another round of risk-off selling, pulling Bitcoin back toward $65,000. On March 27th, a $13.5 billion quarterly options and futures expiry event amplified the downward pressure, as traders closed, rolled, and hedged positions en masse. The nomination of Kevin Warsh as next Federal Reserve Chair had stalled in the Senate amid missing financial disclosures and a Department of Justice investigation into current Chair Jerome Powell — adding Fed leadership uncertainty to an already stressed macro backdrop. By quarter-end, Bitcoin had declined approximately 25% from its January 1st starting point.

The table below places the Q1 2026 performance of DLCF directly alongside the relevant market benchmarks. The contrast is unambiguous.

-3-6.png)

Source: CoinDesk, Santiment, Geco Capital / Figures approximate; crypto prices in USD.

.png)

These numbers tell a story that any investor would recognise as exceptional. In a quarter where Bitcoin lost roughly a quarter of its value and Ethereum lost nearly half, DLCF investors experienced a decline of just 4.26 cents on every euro invested. Put differently, for every €1,000 invested in DLCF at the start of Q1, investors held €957.45 at quarter-end. The same €1,000 held in Bitcoin would have been worth approximately €757. In Ethereum, approximately €562. The capital preservation differential is not marginal — it is transformational.

DLCF outperformed spot Bitcoin by approximately 20 percentage points in Q1 2026 alone. Relative to Ethereum, outperformance exceeded 39 percentage points.

The Q1 2026 result does not exist in isolation. Since inception, the DLCF since its inception (10 Jan 2023) has delivered an all-time cumulative return of 350% — a figure that is particularly meaningful given that this return has been achieved through multiple cycles of extreme volatility, including the prolonged crypto bear market that preceded Bitcoin's October 2025 all-time high. The 350% all-time gain reflects not just the ability to capture upside in bull markets, but critically the ability to defend capital during downturns. The Q1 2026 quarter is perhaps the clearest demonstration yet of that defensive capability.

https://www.gecocapital.ee/digital-large-cap-fund

The DLCF portfolio is structured across three tiers of digital asset exposure. Approximately 80% of the fund is allocated to large-cap digital assets — Bitcoin (BTC), Ethereum (ETH), Tether (USDT), BNB, XRP, USD Coin (USDC), Solana (SOL), TRON (TRX), Chainlink (LINK), and Polygon (MATIC). A further 10% is deployed into mid-cap assets — Polkadot (DOT), Litecoin (LTC), Bitcoin Cash (BCH), Avalanche (AVAX), Stellar (XLM), and Cosmos (ATOM). The remaining 10% is allocated to carefully selected small-cap opportunities including UNI, ETC, EOS, NEO, XEM, and AXS.

Critically, within the large-cap allocation, USDT and USDC — the two largest dollar-pegged stablecoins by market capitalization — are listed holdings. This means the fund's investment mandate explicitly permits the active deployment of a portion of assets into stable, non-volatile instruments when market conditions warrant. In a quarter where every risk asset was being liquidated indiscriminately, the ability to hold stablecoin positions is not a minor tactical advantage — it is a structural buffer that can make the difference between a single-digit drawdown and a catastrophic loss.

DLCF is not a passive index tracker. It is actively managed, with the fund prospectus explicitly stating that investment strategy involves active management of the cryptocurrency basket by a specialised and experienced team. This distinction is fundamental to understanding the Q1 2026 outcome. Passive crypto exposure — whether through a spot ETF, a simple index product, or a directly held portfolio mirroring the market — would have delivered losses in the range of 25–45% during Q1, with no mechanism for mitigation.

Active management, by contrast, allows the fund manager to anticipate deteriorating conditions, rotate into defensive positions, reduce gross exposure, and tactically deploy capital into stablecoins or lower-volatility assets when risk/reward becomes unfavourable. The Q1 2026 result is strong evidence that these tools were employed effectively.

The fund manager, Marcin Wituś, brings 14 years of professional trading experience to the role — an unusually deep credential in a space dominated by operators with far shorter track records. His background includes specialist roles at Citi Bank from 2016 to 2018, where he managed the bank's global foreign exchange position and oversaw options strategies. This experience in managing complex, leveraged positions in traditional financial markets is precisely the kind of pedigree that translates into superior risk management in crypto, particularly during precisely the type of macro-driven selloff that characterised Q1 2026 — where the primary drivers were not crypto-specific, but Federal Reserve policy, tariff dynamics, and geopolitical risk.

DLCF operates with institutional-grade infrastructure. All fund assets are secured on cold wallets — offline storage that eliminates the exchange custody risk that has historically been one of the crypto industry's most catastrophic failure modes. The fund cooperates exclusively with transparent, regulated exchanges, and its scale gives it access to the OTC market — meaning large trades can be executed without the market impact that retail investors face when moving significant capital through public order books. Custody insurance is provided through BitGo, a leading institutional crypto custodian. Exchange access is facilitated through Kraken, one of the longest-established and most transparently regulated cryptocurrency exchanges globally.

These infrastructure choices matter acutely during periods of market stress. During the Q1 2026 sell-off, exchange congestion, forced liquidations on over-leveraged platforms, and withdrawal freezes at less reputable venues created additional losses for retail market participants that DLCF investors were insulated from entirely.

The Q1 2026 crypto market collapse was, at its core, a crisis of over-leverage and over-optimism meeting an unexpectedly hostile macro environment. Markets had entered 2026 pricing in Federal Reserve rate cuts, geopolitical stability, and continued institutional inflows — three assumptions that each proved incorrect within weeks. The four-year Bitcoin halving cycle thesis, which had been one of the market's most widely cited frameworks for predicting 2026 as a peak-performance year, encountered the reality that institutional ownership now means Bitcoin trades as a correlated risk asset during broad deleveraging events, not as an uncorrelated hedge.

On-chain data confirmed the structural weakness beneath the surface. Large whale wallets were selling into January's rally while retail investors bought. Long-term holder net selling peaked at -243,737 BTC in early February. Miner capitulation added further supply to a market already struggling to absorb institutional outflows. The $13.5 billion quarterly derivatives expiry on March 27th demonstrated the extent to which speculative positioning had built up — and how violently it could unwind.

DLCF's outperformance was not a product of luck or timing a single trade correctly. It was the consequence of a management approach that treated capital preservation as a first-order priority — allocating actively into stablecoins when conditions deteriorated, maintaining exposure to assets with the strongest fundamental profiles within the large-cap basket, and refusing to chase momentum into a rally that the underlying on-chain data did not support. The result — a -4.26% quarter in a market that fell 25–45% — speaks directly to the quality of those management decisions.

The same forces that drove Q1 2026's losses are beginning to show early signs of reversal. Long-term Bitcoin holder net selling collapsed by 87% between early February and March 1st — from -243,737 BTC to just -31,967 BTC. Whale cohorts were quietly accumulating during the February and March lows. Bitcoin spot ETF outflows reduced by 94% from November 2025's peak to February 2026. Sovereign-adjacent institutional investors — including Abu Dhabi's Mubadala Investment Company and Al Warda Investments — added spot Bitcoin ETF exposure during the February dip, a strong signal that institutional conviction in the long-term thesis remains intact.

The halving cycle analysis, adjusted for the macro headwinds that delayed its normal timing, continues to point toward meaningful price appreciation in the 12–18 months following Bitcoin's April 2024 halving event — a window that extends well into 2026 and 2027. The Clarity Act regulatory framework, though temporarily delayed, remains an active legislative priority and, when enacted, would represent one of the most significant structural catalysts for the crypto industry's legitimisation in its history.

Within DeFi and the broader altcoin ecosystem, a healthy rotation toward protocols with genuine revenue-generating fundamentals — as evidenced by the strong relative performance of NeoFi protocol baskets and Chainlink's resilience during Q1 — suggests that the next cycle phase will reward quality-focused active management over broad beta exposure. DLCF's portfolio, concentrated in assets with genuine utility, institutional adoption, and network effects, is structurally positioned to benefit from this environment.

For DLCF specifically, the significance of Q1 2026 extends beyond the quarter itself. A fund that preserves capital this effectively during a severe downturn enters the recovery phase with a dramatically stronger compounding position than passive crypto investors who experienced 25–45% losses. At a €45 unit value versus a hypothetical passive-BTC-mirroring unit value of €33–35, DLCF investors begin the recovery with approximately 28–36% more capital to deploy into the next upswing. In an asset class where returns are driven by compounding and where recovery from large drawdowns requires disproportionately large gains, this starting-point advantage is not trivial. It is potentially the difference between fully participating in the next bull market phase and merely recovering to breakeven.

Q1 2026 was a quarter that tested every assumption the cryptocurrency market held about itself. The all-time high was a distant memory. Institutional flows reversed. Macro forces overwhelmed the asset class. Bitcoin fell 25% in three months. Ethereum fell nearly 44%. The total crypto market cap contracted by over a quarter of a trillion dollars. By any measure, it was an environment that revealed who had a real strategy and who had simply benefited from a rising tide.

In that environment, the Geco Capital Digital Large Cap Fund demonstrated exactly what a professionally managed, actively run, institutionally structured crypto investment vehicle is supposed to deliver: meaningful, substantial protection of investor capital during the worst of market conditions, while maintaining the portfolio positioning to capture the upside when conditions improve.

A -4.26% result when the benchmark fell 25%. A capital preservation ratio of nearly 6:1 versus Bitcoin. An all-time gain of 350% through multiple market cycles. DLCF Q1 2026 is a case study in what active management in digital assets can achieve.